The Invisible Line.

The West Valley Fault runs through major cities like Taguig, Pasig, and Muntinlupa. Buying near it scares people. But you need facts, not fear.

The 5-Meter Buffer

The law prohibits building within 5 meters of an active fault trace.

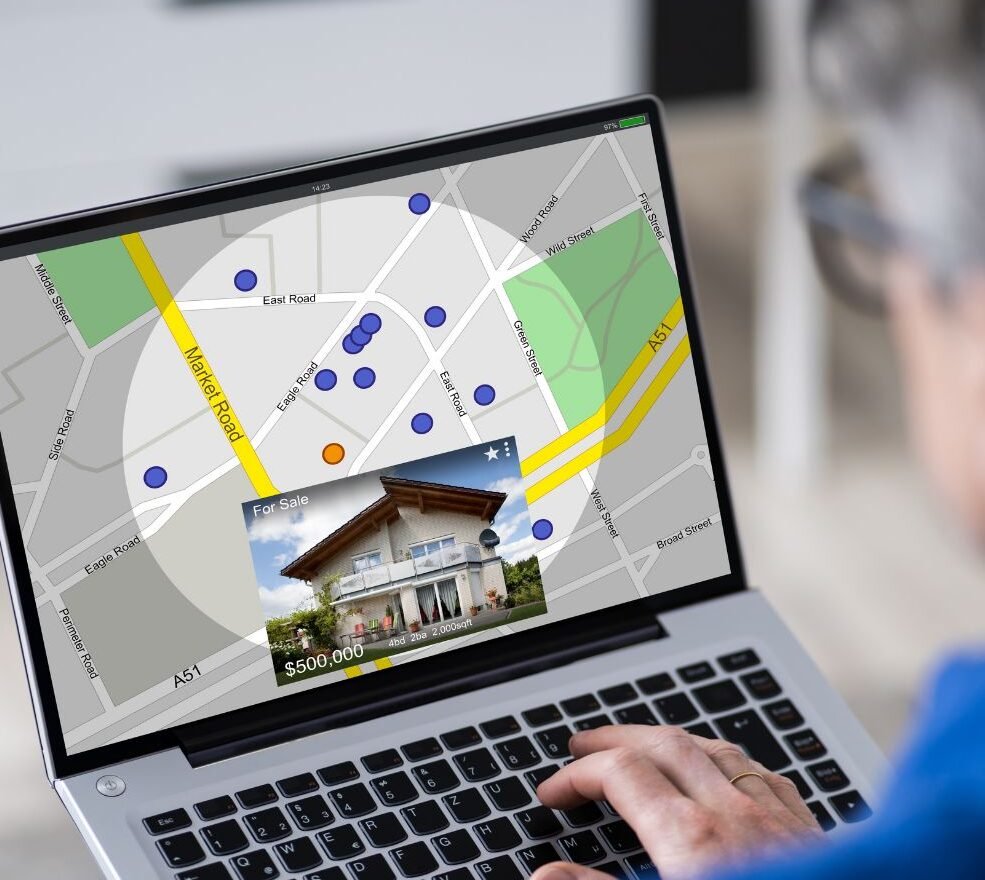

- The Tool: Use the PHIVOLCS FaultFinder app.

- The Reality: If the property is 100 meters away, it is generally compliant. Engineers can design for the shaking; they cannot design for the ground rupturing beneath the foundation.

Knowledge is Power

If a property is flagged near the fault, the price drops. If you confirm it is safely outside the 5-meter zone, you just found a bargain.